Ever picked up your prescription and been shocked that your generic drug cost more than the brand-name version? You’re not alone. Many people assume generics are always the cheapest option - but that’s not true anymore. Thanks to how insurance plans are structured, your generic medication could be sitting in a higher tier, costing you $30, $50, or even more per month - even though it’s chemically identical to the cheaper version just a few slots down.

How Tiered Copays Work

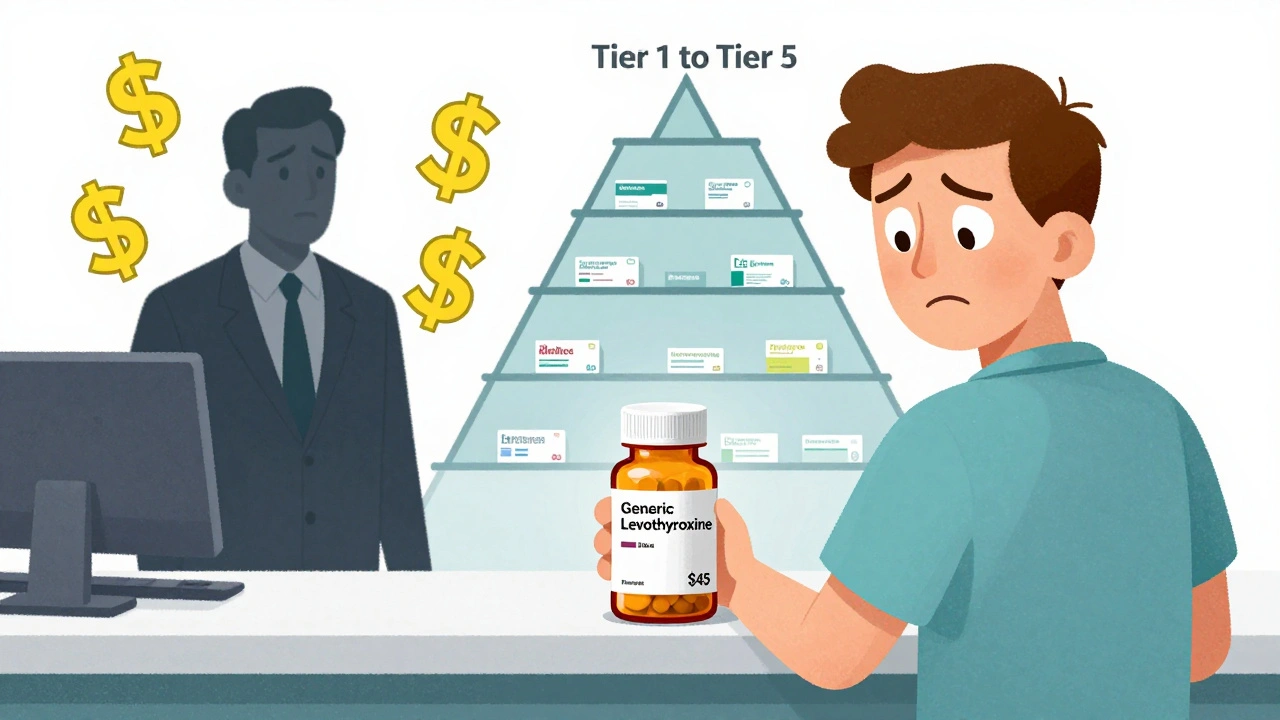

Most health plans today use something called a tiered formulary. Think of it like a pricing ladder for drugs. Each tier has a different copay amount, and where your drug lands determines how much you pay out of pocket. The system was designed in the late 1990s by Pharmacy Benefit Managers (PBMs) like CVS Caremark, Express Scripts, and OptumRx to control rising drug costs. The idea was simple: make cheaper, preferred drugs easier to afford, and make expensive or non-preferred ones harder to justify. Here’s how the typical tiers break down:- Tier 1: Preferred generics - usually $0 to $15 for a 30-day supply.

- Tier 2: Preferred brand-name drugs - $25 to $50.

- Tier 3: Non-preferred brand-name drugs - $60 to $100.

- Tiers 4 and 5: Specialty drugs - often 20% to 40% coinsurance, sometimes hundreds or thousands per month.

Why Your Generic Isn’t in Tier 1

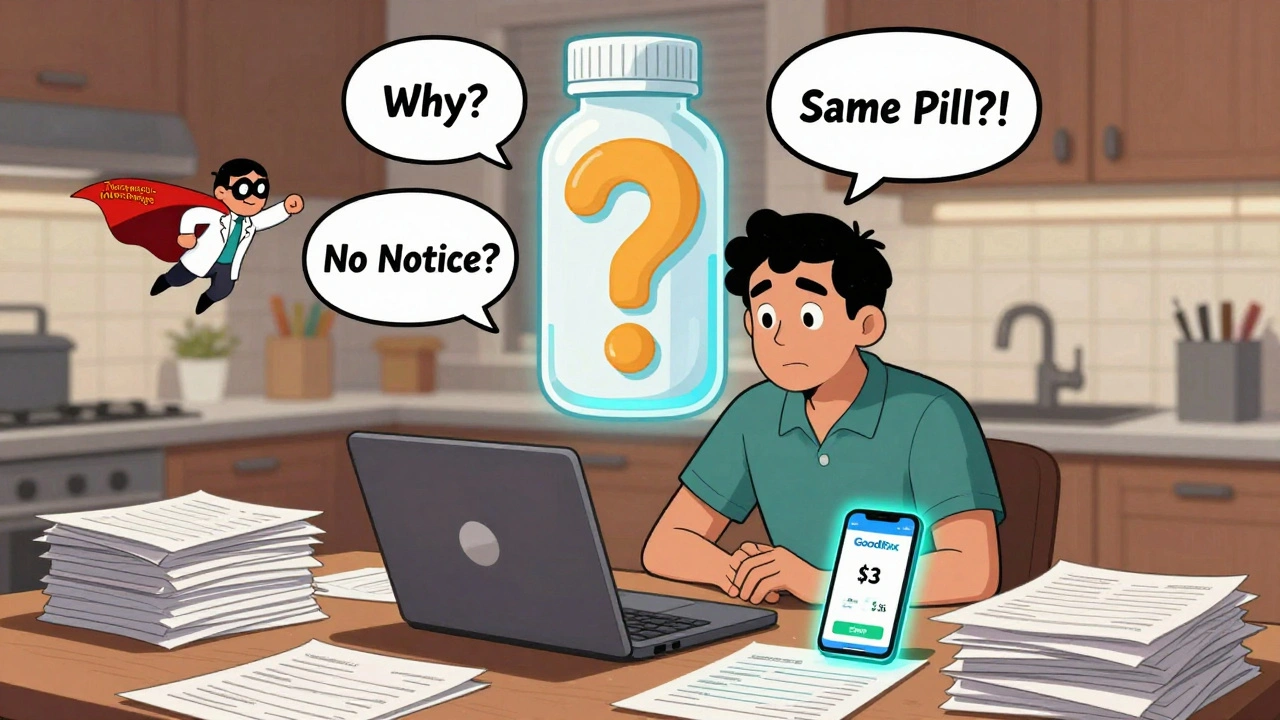

It’s not about effectiveness. It’s not about safety. It’s not even about which version your doctor recommends. The only thing that determines whether your generic lands in Tier 1 or Tier 3 is money. Specifically, the rebate the drug manufacturer pays to the PBM. PBMs negotiate these deals behind closed doors. If one generic maker offers a $2 rebate per pill and another offers $0.50, the PBM will push the higher-rebate version into Tier 1 - even if both are the exact same medicine. Dr. Dennis G. Smith, former director of the Center for Medicaid and CHIP Services, put it plainly: “Preferred status has nothing to do with clinical superiority - it’s entirely about the rebates and discounts PBMs negotiate with manufacturers.” This isn’t theoretical. In 2024, Express Scripts moved 87 generic drugs to higher tiers simply because their rebate contracts expired. One patient on Reddit reported their levothyroxine - a generic thyroid medication millions take - jumped from $5 to $45 overnight. Their doctor confirmed: all versions are identical. The insurer wouldn’t explain why.The Confusion Factor

Patients don’t expect this. When you hear “generic,” you assume “cheapest.” But insurance plans don’t label drugs that way. They use terms like “preferred” and “non-preferred” - terms most people don’t understand. A 2023 survey by the Patient Advocate Foundation found that 41% of insured adults had experienced a generic drug costing more than they expected. Of those, 68% said they couldn’t get a clear answer from their insurer. On patient forums, common complaints include:- Getting a different generic pill than usual - and paying more.

- Pharmacists automatically switching your prescription to a non-preferred version without telling you.

- Being told your drug moved tiers mid-year with no notice.

What You Can Do

You don’t have to accept this. Here’s how to fight back:- Check your formulary - every October, Medicare plans update theirs. Commercial plans often change mid-year too. Log into your insurer’s website and search for your drug. Look for the tier label.

- Ask your pharmacist - they know which generics are preferred. Ask: “Is there another version of this drug that’s cheaper?” Sometimes they can switch you to the Tier 1 version without a new prescription.

- Request a therapeutic interchange - this is a form your doctor can sign to get your drug moved to a lower tier. In 2024, 63% of these requests were approved.

- Use cost tools - GoodRx, SmithRx, and Humana’s Drug Cost Lookup show real-time prices across pharmacies. Sometimes the cash price is lower than your copay.

- Appeal - if your drug was moved to a higher tier, you can file an exception. You’ll need a letter from your doctor saying the change harms your health. Urgent appeals must be processed within 72 hours.

- Check manufacturer programs - many drugmakers offer coupons or patient assistance programs. In 2023, these covered 22% of specialty drug costs for eligible patients.

Specialty Generics Are the New Wild West

The biggest surprise? Some generics are now considered specialty drugs. These are usually biologics - complex medications made from living cells - that now have generic versions called biosimilars. Examples include adalimumab (used for rheumatoid arthritis) and insulin glargine. Even though these are technically generics, they’re placed in Tier 4 or 5 because they cost $5,000 to $10,000 a month. Your coinsurance might be 30% - meaning you pay $1,500 to $3,000 per month. And yes, your insurer can switch you to a different biosimilar without telling you, and it could cost you hundreds more.

What’s Changing in 2025

The Inflation Reduction Act kicks in January 2025, capping out-of-pocket drug costs at $2,000 per year for Medicare Part D enrollees. That’s huge - but it doesn’t change tier structures. You’ll still pay more for non-preferred drugs until you hit the cap. Meanwhile, PBMs are already adjusting. UnitedHealthcare moved popular generics like atorvastatin and lisinopril to $0 copays in Tier 1 to attract more members. But less common generics? They’re being pushed to Tier 2 with $10 copays. The goal? Keep the system complex enough to control spending - but simple enough to avoid backlash.Bottom Line

Your generic drug isn’t cheaper because it’s better. It’s cheaper because the manufacturer paid more to the middleman. And if that deal ends, your price can spike overnight - with no warning, no explanation, and no clinical reason. The system works for insurers and PBMs. It doesn’t work for patients. But you have more power than you think. Know your formulary. Ask questions. Push back. And don’t let a rebate contract decide your health.Why is my generic drug more expensive than the brand-name version?

It’s not about the drug - it’s about the rebate. Your generic might be in a higher tier because the manufacturer didn’t pay a big enough discount to your insurer’s Pharmacy Benefit Manager (PBM). Even if it’s chemically identical to a cheaper version, the PBM puts the one with the best rebate in Tier 1. The brand-name drug might be in a lower tier if its manufacturer pays a large rebate, making it cheaper than your generic.

Can my insurer change my drug’s tier without telling me?

Yes. Insurers can update their formularies at any time, though Medicare plans must notify members by October 1 for changes starting January 1. Commercial plans often change mid-year with little notice. You may only find out when your pharmacy says your copay went up. Always check your formulary annually and monitor your Explanation of Benefits (EOB) statements.

Are all generic versions of a drug the same?

Yes, legally. The FDA requires generic drugs to have the same active ingredient, strength, dosage form, and route of administration as the brand-name drug. They must also meet the same quality and performance standards. Differences in inactive ingredients (like fillers or dyes) rarely affect how the drug works. If your doctor says all generics are the same, they’re right - but your insurer doesn’t care. They care about rebates.

What’s the difference between a preferred and non-preferred generic?

There’s no clinical difference. “Preferred” means the manufacturer paid a better rebate to your insurer’s PBM. “Non-preferred” means they didn’t. It’s purely a financial decision. Your doctor can’t tell which version is preferred - only your insurer’s formulary can. Always ask your pharmacist: “Is there a preferred generic for this?”

How do I find out what tier my drug is on?

Log into your insurance plan’s website and look for the “Drug Formulary” or “Prescription Drug List.” Search for your drug by name. It will show the tier (Tier 1, Tier 2, etc.) and your copay amount. You can also call your insurer’s pharmacy help line or ask your pharmacist to check. Third-party tools like GoodRx and SmithRx can also show tier info and compare prices across pharmacies.

Can I switch to a different generic to save money?

Yes - but you need your doctor’s help. Ask your doctor to write a new prescription for the preferred generic version. If they’re unsure which one is cheaper, your pharmacist can help. You can also request a “therapeutic interchange” form, which your doctor signs to get your drug moved to a lower tier. This works 63% of the time, according to 2024 Medicare data.

Do all insurance plans use tiered copays?

Almost all. As of 2024, 98% of employer-sponsored plans and 99% of Medicare Part D plans use tiered formularies. Only a small number of older or very basic plans still use flat copays. Tiered systems are now the industry standard because they help insurers control spending - even if they confuse patients.

Will the $2,000 out-of-pocket cap in 2025 fix this problem?

No - it caps your total spending, but doesn’t change how tiers work. You’ll still pay more for non-preferred drugs until you hit the $2,000 limit. If you take expensive medications, you’ll likely hit the cap quickly. But if you take a few generics, you might pay more upfront because your preferred drug is in Tier 1 and your non-preferred one is in Tier 3. The cap helps with total cost, not fairness.

Comments (8)