When you pick up a generic drug copay, the fixed amount you pay out-of-pocket for a generic medication covered by your insurance plan. Also known as a prescription copayment, it’s one of the most direct ways your insurance controls drug spending. But here’s the thing—your copay isn’t set in stone. It changes based on your plan, the pharmacy you use, and even the drug’s tier on your insurer’s list. Not all generics cost the same to you, even if they’re chemically identical.

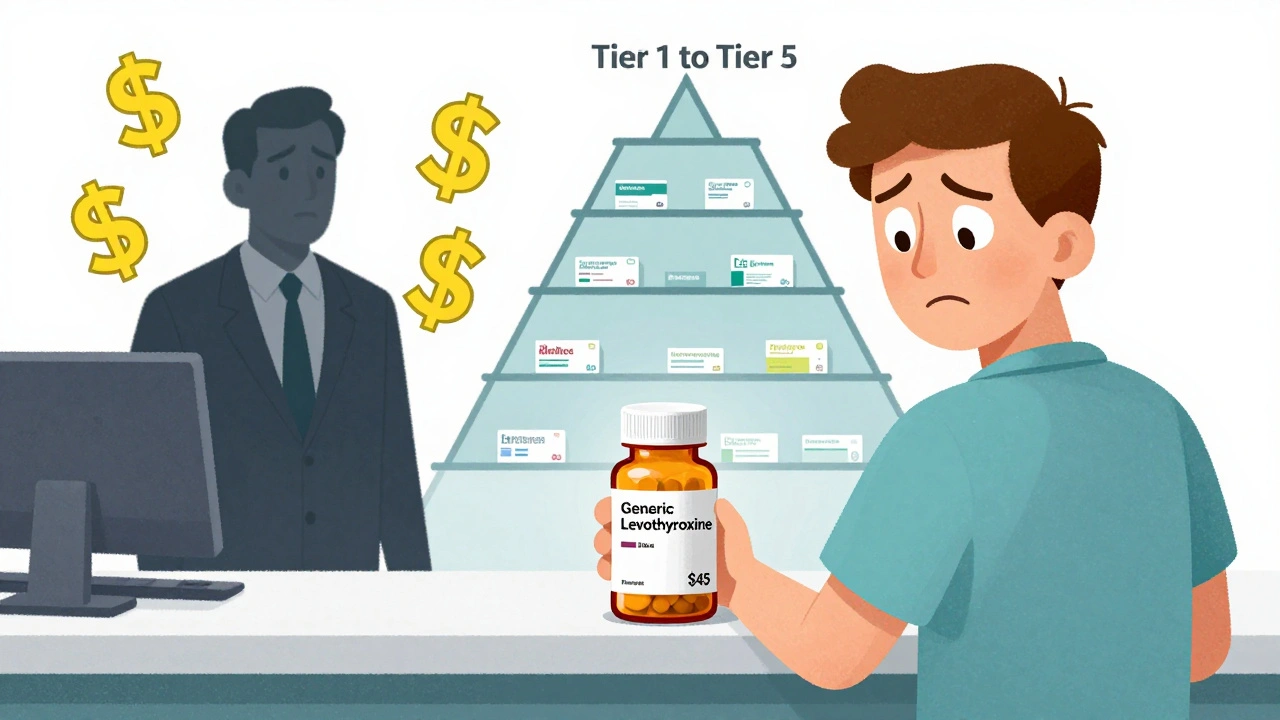

Why does this happen? Because insurance companies group drugs into tiers, categories that determine how much you pay. Tier 1 is usually the cheapest—often $5 or $10 for generics. Tier 2 might be $15 to $25. Some plans even put certain generics in Tier 3 or higher if they’re newer, more popular, or if the manufacturer pays the insurer to promote them. That’s right—sometimes a generic costs more than a brand-name drug because of how the deal was structured between the pharmacy benefit manager and the maker.

And it’s not just about the drug itself. Your pharmacy copay, the amount you pay at the counter for any prescription depends on where you fill it. A mail-order pharmacy might charge $10 for a 90-day supply. A local pharmacy could charge $20 for the same thing. Some plans even have different copays for in-network vs. out-of-network pharmacies. If you’re paying more than you should, you’re not alone—most people don’t realize they can shop around.

Then there’s the insurance drug coverage, the rules your plan uses to decide which drugs it pays for and how much. Some plans require prior authorization before they’ll cover even a basic generic. Others won’t pay unless you’ve tried a cheaper alternative first. And if you’re on Medicare Part D, your copay can change every year based on the plan’s formulary update. You’re not just paying for the pill—you’re paying for the system around it.

But here’s the good news: you have more control than you think. You can ask your pharmacist if a different generic version is cheaper. You can check if your plan has a preferred pharmacy network. You can use apps or websites to compare prices across nearby pharmacies—even for the same generic. Some stores like Walmart and Costco sell common generics for under $5 without insurance. And if your copay is too high, talk to your doctor. Sometimes switching to a different generic—or even a brand drug that’s on a lower tier—can save you money.

The posts below cover exactly this: how generic drugs are priced, how insurers decide what you pay, and how real people cut their medication costs without risking their health. You’ll find guides on how to read your drug formulary, what to ask your pharmacist, and why some generics cost more than others—even when they’re made by the same company. You’ll also see how regulatory rules, like FDA approval and therapeutic equivalence codes, affect what ends up on your receipt. No fluff. Just what you need to know to pay less and get the right medicine.

Written by Mark O'Neill

Why your generic drug might cost more than the brand-name version - it's not about the medicine, it's about rebates. Learn how tiered copays work and what you can do to save money.